Which of the following properties are not eligible for like kind exchange under 1031?

Under IRC §1031, the following properties do not qualify for tax-deferred exchange treatment: Stock in trade or other property held primarily for sale (i.e. property held by a developer, “flipper” or other dealer) Foreign real property for U.S. real property. Goodwill of one business for goodwill of another business.

Which properties do not qualify for a like kind exchange?

Securities, stocks, bonds, partnership interests, and other financial assets are excluded from the definition of like-kind property. Securities, stocks, bonds, partnership interests, and other financial assets are not considered like-kind properties and are exempt from tax deferrals.

What is a like kind exchange of property?

A like-kind exchange is a tax-deferred transaction that allows for the disposal of an asset and the acquisition of another similar asset without generating a capital gains tax liability from the sale of the first asset.

How does a 1031 exchange work with rental properties?

The intermediary holds the funds after one property is sold in the 1031 exchange and uses that money to buy the new replacement property. When doing a 1031 exchange, the owner must identify the property he is exchanging and declare it before the sale.

What does 1031 mean for like kind property?

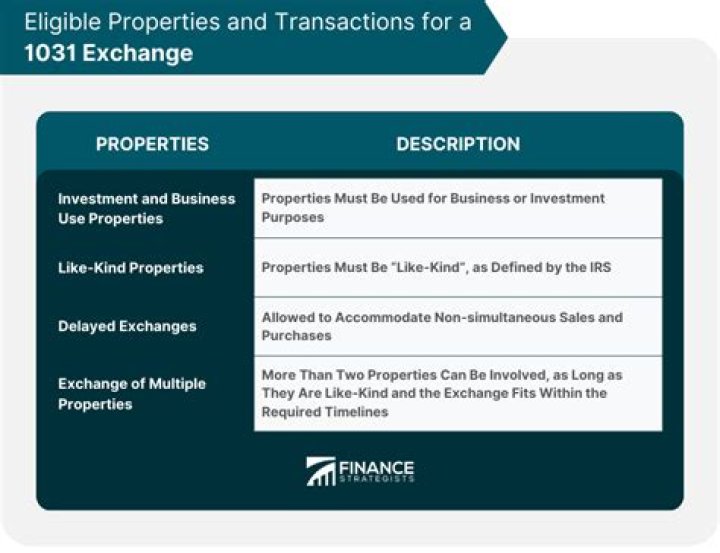

In a typical IRS qualified §1031 like-kind property exchange, investors defer paying capital gains, depreciation recapture, and income taxes on commercial investment property when it’s sold. Like-kind does not mean identical property, but it certainly excludes (with a twist) exchanges for primary residences.

Who is the owner of an exchange property?

Regardless of whether the old property is owned by a corporation, an S-Corp., an LLC, a partnership or a trust, the taxpayer that owns the old property is the same one that must do the exchange and take title to the new property.

Do you have to pay taxes on 1031 exchange?

When using 1031 tax codes, you could continue to exchange properties for as long as you want. Ultimately, however, you would need to pay the taxes on these properties. When you decide to sell one of the like-kind properties, you would need to pay relevant taxes as well as all of the taxes that were tax-deferred throughout your exchanges.