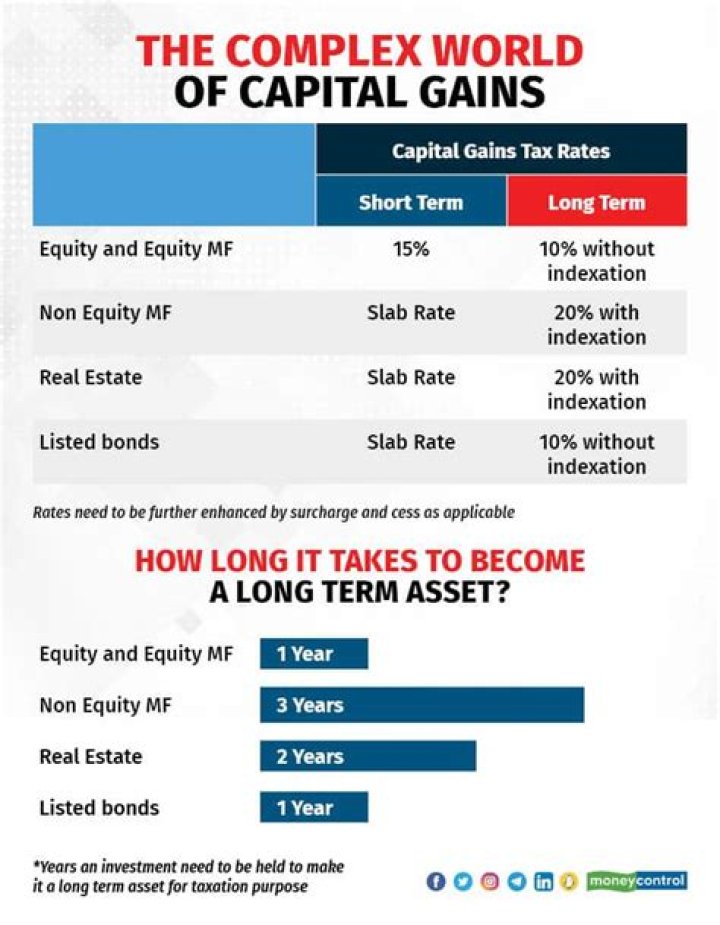

What is the holding period for long-term capital gains and losses?

one year

Generally, if you hold the asset for more than one year before you dispose of it, your capital gain or loss is long-term. If you hold it one year or less, your capital gain or loss is short-term.

Can net long-term capital losses offset ordinary income?

Deducting Capital Losses If you don’t have capital gains to offset the capital loss, you can use a capital loss as an offset to ordinary income, up to $3,000 per year. (If you have more than $3,000, it will be carried forward to future tax years.)

Do ordinary gains and losses affect net income?

Ordinary Losses for Taxpayers An ordinary loss will offset ordinary income and capital gains on a one-to-one basis. Net your long-term capital gains and losses. $3,000 – $14,000 = $11,000 net long-term capital loss. Net your net short-term and long-term capital gains and losses.

The holding period of an investment is used to determine the taxing of capital gains or losses. A long-term holding period is one year or more with no expiration. Any investments that have a holding of less than one year will be short-term holds. The payment of dividends into an account will also have a holding period.

Can long-term capital gains be offset by business losses?

Can I deduct my capital losses? Yes, but there are limits. Losses on your investments are first used to offset capital gains of the same type. So, short-term losses are first deducted against short-term gains, and long-term losses are deducted against long-term gains.

When to use long term capital gains or losses?

To correctly arrive at your net capital gain or loss, capital gains and losses are classified as long-term or short-term. Generally, if you hold the asset for more than one year before you dispose of it, your capital gain or loss is long-term.

How to report capital gains and losses on Form 1040?

Report most sales and other capital transactions and calculate capital gain or loss on Form 8949, Sales and Other Dispositions of Capital Assets, then summarize capital gains and deductible capital losses on Schedule D (Form 1040), Capital Gains and Losses.

Is there limit on carryover of capital gains?

Limit on the Deduction and Carryover of Losses. If your capital losses exceed your capital gains, the amount of the excess loss that you can claim to lower your income is the lesser of $3,000 ($1,500 if married filing separately) or your total net loss shown on line 16 of the Form 1040, Schedule D (PDF).

What does it mean to have a net capital gain?

If you have a net capital gain, a lower tax rate may apply to the gain than the tax rate that applies to your ordinary income. The term “net capital gain” means the amount by which your net long-term capital gain for the year is more than your net short-term capital loss for the year.