What is a report of Income Tax Examination Changes?

Form 4549, Income Tax Examination Changes, is used for cases that result in: Normally, the IRS will use the form for the initial report only, and the IRS reasonably expects agreement. Adjustments to income or deduction items don’t affect or warrant a change in tax liability or refundable credits on the return audited.

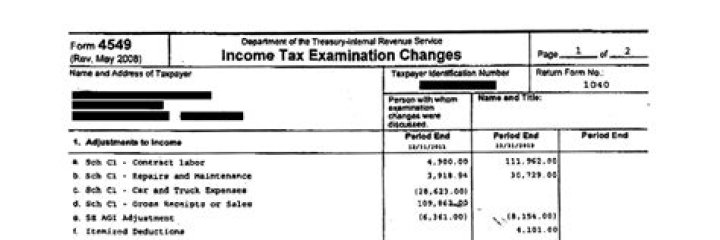

What is a 4549?

An IRS Form 4549 is a “Statement of Income Tax Examination Changes.” This is merely a proposed adjustment if it is attached to a Letter 525, 692 or 1912. However, if Form 4549 is attached to a Notice of Deficiency then the IRS has made a final determination that you owe the tax.

What is a tax form 4549?

The IRS Form 4549 is the Income Tax Examination Changes Letter. The Form will include a summary of the proposed changes to the tax return, penalties, and interest determined as an outcome of the audit. It will include information, including: Adjustments to Income. Total Adjustments.

When is a tax return selected for examination?

A return selected for examination is considered as surveyed before assignment if it is disposed of before contact with taxpayers and prior to assignment to an examiner. A team manager will survey returns before assignment if no examination is warranted.

What are the procedures for an IRM 4.10 examination?

IRM 4.10, Examination of Returns, provides the basic procedures, guidelines and requirements for use by revenue agents, tax compliance officers, tax auditors and tax examiners in conducting income tax examinations. Additional procedures for LB&I cases are found in IRM 4.46, LB&I Examination Process.

How to conduct an Internal Revenue Service examination?

Provide accurate and complete information. Be courteous and professional, regardless of the opposing party’s behavior. Steer the direction of the conversation, remaining focused on the purpose of the call. Take ownership of the call and address issues raised. Make helpful and productive referrals, as applicable.

Why was IRM 4.63.4.11, report writing amended?

(2) IRM 4.63.4.11, Report Writing. was updated to coincide with the revision to IRM 4.10.8, Examination of Returns, Report Writing. Paragraphs relating to the use of fax in taxpayer submissions were removed because this subject is addressed in IRM 4.10.8.2.4.2. Paragraphs in the subsection were rearranged to improve logical flow.