What happens if I pull out of a refinance?

You can back out of a home refinance, within a certain grace period, for any reason, but you may face a fees or penalty if you choose to cancel or otherwise can’t refinance. When a refinance doesn’t go through, you typically must cut your losses for certain up-front costs you paid during the refinance process.

How much money can you pull out on a refinance?

How much money can I get from a cash-out refinance? While lenders typically allow homeowners to borrow up to 80 percent of the home’s value, the threshold can vary depending on your credit score and type of mortgage.

How long does a refinance take without appraisal?

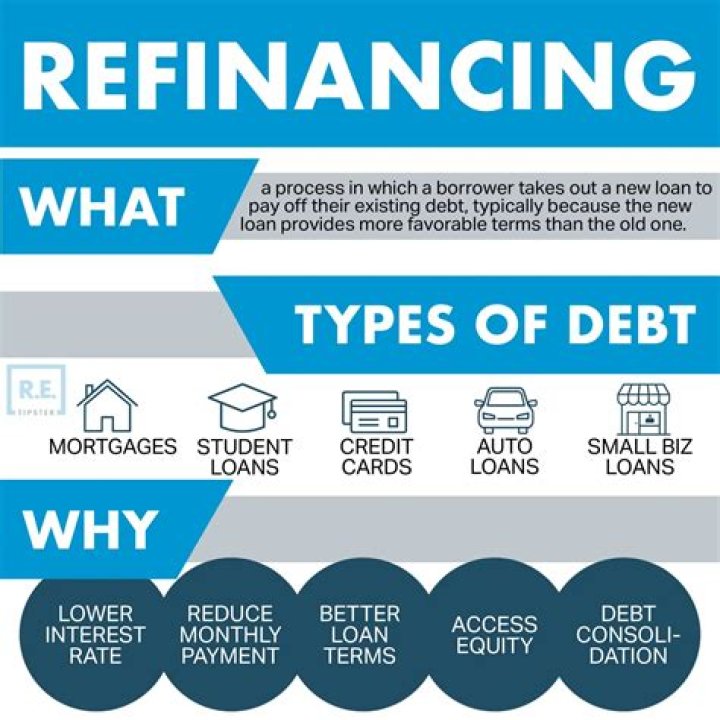

A refinance typically takes 30 – 45 days to complete. However, no one will be able to tell you exactly how long yours will take. Appraisals, inspections and other third parties can delay the process. Your refinance might be longer or shorter, depending on the size of your property and how complicated your finances are.

Can I back out of a refinance after closing?

If you are buying a home with a mortgage, you do not have a right to cancel the loan once the closing documents are signed. If you are refinancing a mortgage, you have until midnight of the third business day after the transaction to rescind (cancel) the mortgage contract.

Can you sue a refinancing company?

The lender liability lawyers at MahanyLaw and Judge, Lang & Katers have joined forces to sue banks, lenders, mortgage companies and loan servicers. If you have been denied a promised refinancing, you may have legal rights and claims against the bank.

How soon can you cash-out refinance?

six months

Rules for cash-out refinances Most lenders make you wait a minimum of six months after the closing date before you can take cash out on a conventional mortgage. If you have a VA-backed mortgage, you must have made a minimum of six consecutive payments before you can apply for a cash-out refinance.

Can I walk away from a refinance?

You can walk away from a bad deal even at the last minute. Refinancing involves great potential for hidden costs, fees, security interests and other unfair loan terms. Even some reputable lenders make unfair refinancing deals.

What can stop a refinance?

6 common reasons a refinance is denied

- You have too much debt.

- You have bad credit.

- Your home has dropped in value.

- Your application was incomplete.

- Your lender can’t verify your information.

- You don’t have enough cash.

How do I dispute my mortgage debt?

If you’re requesting information, your servicer can: If you have a problem with your mortgage, you can submit a complaint online or by calling (855) 411-CFPB (2372). If you’re facing imminent foreclosure or have been served with legal papers, you may also need to consult an attorney.

How to avoid getting ripped off by a mortgage broker?

Search Tap on the profile icon to edityour financial details. Got It 3 Ways to Avoid Getting Ripped Off By Mortgage Brokers Rebecca LakeJun 25, 2018 Share Enlisting the help of a mortgage broker can make the home buying process run more smoothly.

How to avoid being ripped off by a car dealer?

A reliable way to avoid being scammed or ripped off by a dealer is to arrange your own financing and to know your credit score. Arrange your financing. Browse our guide on car loans before visiting a dealership to get your financing in order — it gives you more negotiating power and could help you lower the cost of your purchase.

What happens when you stop making payments to a loan modification company?

According to the FTC, victims of loan modification scams are often told to stop making payments to their lender because the loan modification company is going to take care of negotiations. This never happens, and the victim can’t get in contact with the company after paying for the service.