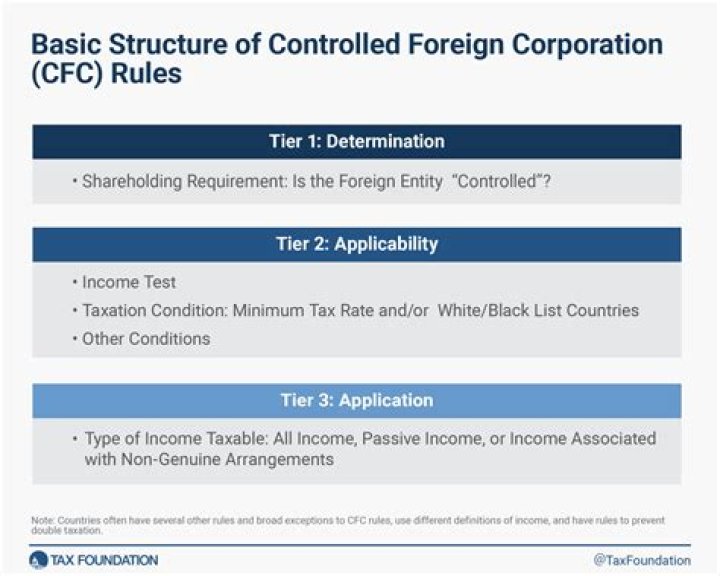

What are the requirements for a foreign corporation to be a controlled foreign corporation for US tax purposes?

To be considered a controlled foreign corporation in the U.S., more than 50% of the vote or value must be owned by U.S. shareholders, who must also own at least 10% of the company.

What is the difference between a domestic foreign and alien corporation?

Domestic Corporation: A corporation incorporated in a given state and doing business in that same state. Alien Corporation: A corporation doing business in a given state, but incorporated in (or otherwise formed, as provided for by the laws thereof) a foreign country.

Under U.S. tax law, if a foreign corporation is a “Controlled Foreign Corporation” (“CFC”), then a “United States Shareholder” who owns stock in the corporation on the last day of the taxable year is required to include in its gross income for the taxable year certain “deemed” income, primarily – such person’s pro-rata …

What is Subpart F of controlled foreign corporations?

Subpart F deals with the U.S. taxation of amounts earned by controlled foreign corporations (CFCs). It provides that certain types of income of CFCs, though undistributed, must be included in the gross income of the U.S. shareholder in the year the income is earned by the CFC.

How are dividends taxed in a controlled foreign corporation?

Dividends are generally taxed in the year they are received. In addition, there may be some Subpart F income for the controlled foreign corporation — even in years when no income was distributed. In order for a Foreign Corporation to be considered a Controlled Foreign Corporation, it must be owned more than 50% by U.S. Persons.

What are the rules for Subpart F income?

Subpart F Income & Controlled Foreign Corporations (CFC): The IRS Rules for Subpart F Income, CFC, and U.S. Shareholder Foreign Earnings are very complicated. Essentially, Subpart F Income involves CFCs ( Controlled Foreign Corporations) that accumulate certain specific types of income (primarily passive income).

Can a CFC be taxed under Subpart F?

Under Subpart F rules and IRC 952 , U.S. shareholders of a CFC may be taxed on certain foreign corporation income, even if it has not been distributed. The income attributed to them is based on their ratable share.