Is a 457 a retirement account?

457 plans are IRS-sanctioned, tax-advantaged employee retirement plans. They are offered by state, local government, and some nonprofit employers. Participants are allowed to contribute up to 100% of their salary, provided it does not exceed the applicable dollar limit for the year.

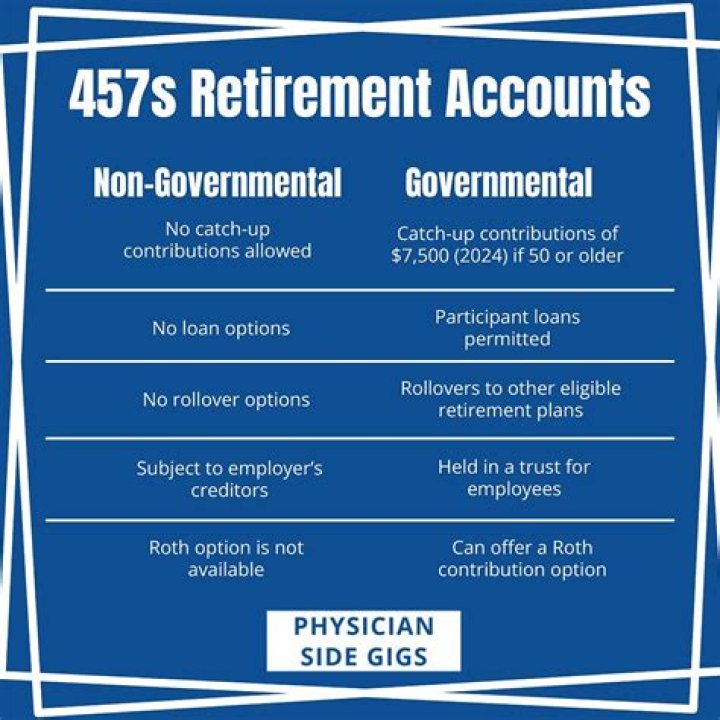

What type of account is a 457?

A 457(b) is a type of tax-advantaged retirement plan for state and local government employees, as well as employees of certain non-profit organizations.

What is a 457 b retirement account?

457 Plans. By comparison, 457(b) plans are IRS-sanctioned, tax-advantaged employee retirement plans offered by state and local public employers and some nonprofit employers. 4 They are among the least common forms of defined-contribution retirement plans.

Why should I do deferred compensation?

Deferred compensation plans also reduce the current year’s tax burden on employees. When a person contributes to a deferred compensation plan, the amount contributed over the year reduces taxable income for that year, therefore reducing the total income taxes paid.

What kind of retirement plan is a 457 plan?

457 plans are non-qualified, tax-advantaged, deferred compensation retirement plans offered by state, local government and some nonprofit employers.

What is the CalPERS 457 supplemental income plan?

The CalPERS Supplemental Income 457 Plan (CalPERS 457 Plan) provides employees a low-cost, convenient way to save for retirement through payroll deductions.

Is there an administrative fee for a 457 plan?

The employee pays a $1.50 monthly administrative fee for each plan account. Employees may enroll in both the 401 (k) and 457 (b), but that also means they will pay administrative fees for both. For that reason, most employees maximize contributions to one plan before they open up a second plan account.

What’s the catch up provision in a 457 plan?

Also, 457 (b) plans feature a “double limit catch-up” provision. This is designed to allow participants who are nearing retirement to compensate for years in which they did not contribute to the plan but were eligible to do so.