How long does it take to get annuity payout after death?

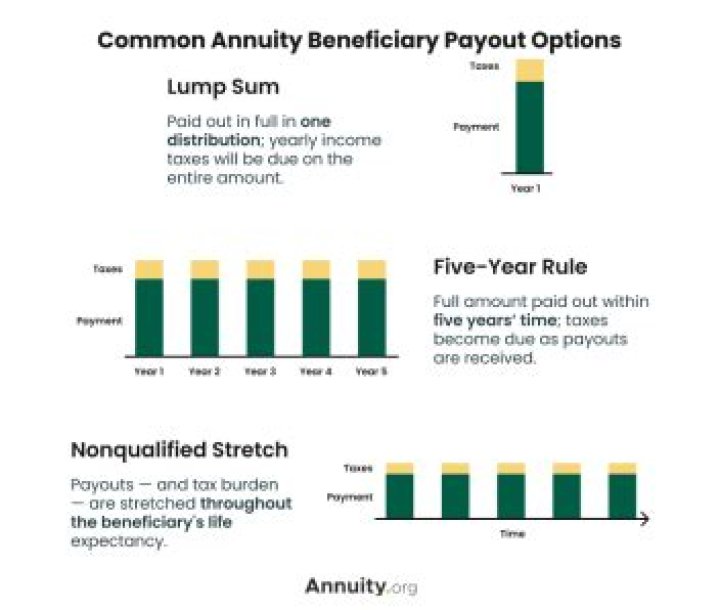

Five-Year Rule. The beneficiary or beneficiaries of an annuity have five years to take out the proceeds. They can take them out gradually or in a single lump sum anytime, as long as they withdraw all of the death benefit with 5 years of the annuitant’s death.

The beneficiary or beneficiaries of an annuity have five years to take out the proceeds. They can take them out gradually or in a single lump sum anytime, as long as they withdraw all of the death benefit with 5 years of the annuitant’s death.

How are death benefits paid out in annuities?

Heirs can take an annuity death benefit as a lump sum payment or as regular payouts. Death Benefit Amounts. Generally, there are two ways to determine a standard annuity death benefit. First, you can pay out any remaining assets to your beneficiary. Say you purchased a $500,000 annuity and it paid out $300,000 during your lifetime.

What happens to a joint life annuity when the beneficiary dies?

On the death of an annuitant, a joint life annuity will continue to be paid to the survivor for the rest of the survivor’s lifetime – and the survivor doesn’t need to be a dependant. However, the annuity provider may restrict this, say to a named beneficiary.

Do you need a death certificate to claim an annuity?

Most annuity companies require more than just the completed forms to process your claim. You must provide a certified copy of the decedent’s death certificate with the cause-of-death information on it. The company may require that your signature be notarized before it will accept the claim form.

Do you have to pay taxes on death benefits?

Annuity beneficiaries may pay income or capital gains tax on death benefits they receive, but these benefits don’t have to go through probate. If you already own or are considering purchasing a VA with M&E fees, here are a couple of strategies to consider.