How is the alternative minimum tax system different from the regular income tax system?

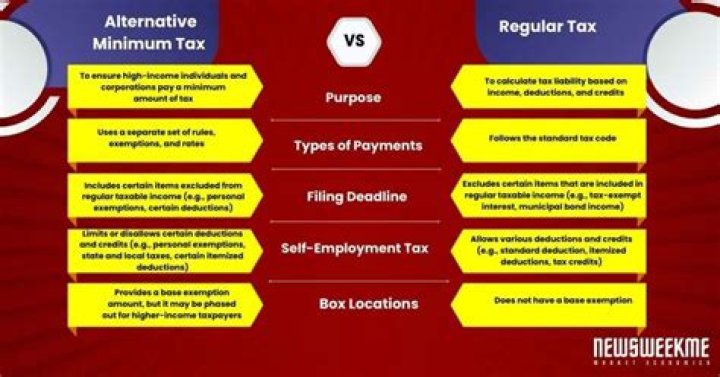

The AMT system doesn’t allow the same deductions and adjustments, and it may consider different forms of income as taxable. For example, the regular tax system might exclude income from certain types of municipal bonds, while the AMT considers this income taxable.

Is alternative minimum tax double taxation?

Incomes above the annual AMT exemption amounts typically trigger the alternative minimum tax. AMT payers, who typically have relatively high incomes, essentially calculate their income tax twice — under regular tax rules and under the stricter AMT rules — and then pay the higher amount owed.

Who is subject to the alternative minimum tax?

The AMT increased taxes for 23.3 percent of households with “expanded cash income” (a broad measure of income) between $200,000 and $500,000, 63.8 percent of those with incomes between $500,000 and $1 million, and 24.2 percent of households with incomes greater than $1 million (table 1).

How is the amount of the alternative minimum tax determined?

The AMT recalculates income tax after adding certain tax preference items back into adjusted gross income. Preferential deductions are added back into the taxpayer’s income to calculate his or her alternative minimum taxable income (AMTI), and then the AMT exemption is subtracted to determine the final taxable figure.

What is AMT exemption phase?

exemption phase-out, the loss of the exemption raises the taxpayer’s effective AMT tax rate. This occurs because for each $1 of income in the phase-out range, the amount of AMTI actually subject to tax increases by $1.25. This results in an effective AMT rate of 35% (instead of 28%) for AMTI in the phase-out range.

What are the benefits of the Alternative Minimum Tax?

Under the tax law, certain tax benefits can significantly reduce a taxpayer’s regular tax amount. The alternative minimum tax (AMT) applies to taxpayers with high economic income by setting a limit on those benefits. It helps to ensure that those taxpayers pay at least a minimum amount of tax.

How is the Alternative Minimum Tax ( AMT ) calculated?

The alternative minimum tax (AMT) applies to taxpayers with high economic income by setting a limit on those benefits. It helps to ensure that those taxpayers pay at least a minimum amount of tax. How Is the AMT Calculated?

When was the Alternative Minimum Tax signed into law?

Back in 1969, the U.S. Secretary of the Treasury realized that 155 taxpayers who earned well into six figures (in 1960s dollars) did not pay any income tax at all. They avoided it by claiming so many tax deductions that they were effectively erasing their incomes. The AMT was signed into law a year later to prevent this.

What’s the difference between AMT and ordinary income tax?

The Alternative Minimum Tax (AMT) is a separate tax system that requires some taxpayers to calculate their tax liability twice—first, under ordinary income tax rules, then under the AMT—and pay whichever amount is highest. The AMT has fewer preferences and different exemptions and rates than the ordinary system.