How do I calculate capital gains on my primary residence?

Subtract your basis from your proceeds to calculate your gain on the sale of your personal residence. In this example, subtract $330,000 from $950,000 to find your gain equals $620,000. Subtract your primary residence exclusion from the taxable gain.

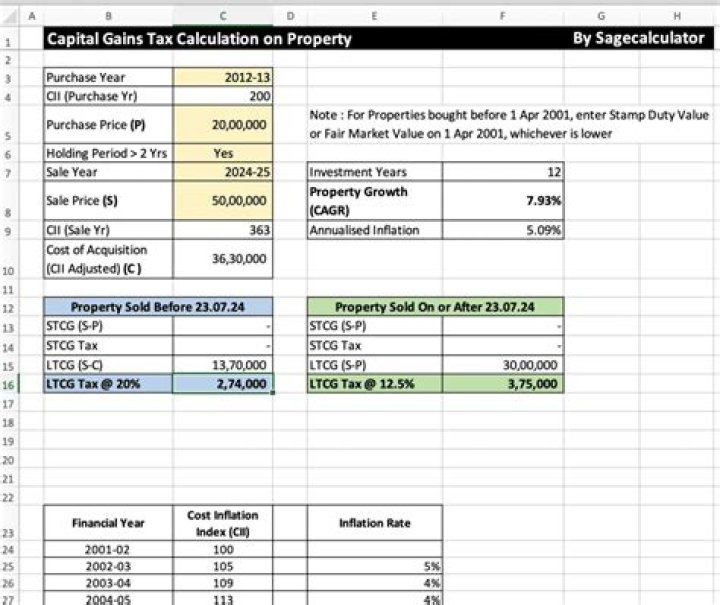

How do you calculate capital gains on sale of residential property?

This can be calculated by multiplying the purchase price of the house, which is Rs 45,00,000 with the indexation factor of 1.52….Illustrative Example for Long Term Capital Gain Tax on Sale of a House.

| Particulars | Amount in Rupees |

|---|---|

| Sale price of the house | 95,00,000 |

How is primary residence excluded from capital gain on assessment?

SARS will then apply the R 2 million primary residence exclusion to the capital gain on assessment. If the property sold was not your primary residence (example 2), tick the No block in the section which asks this question. The primary residence exclusion will not be applied to this transaction when you’re assessed.

What are the tax benefits of being a primary residence?

Your primary residence may also qualify for income tax benefits: both the deduction of mortgage interest paid as well as the exclusion of profits from capital gains tax when you sell it. Because of the tax benefits, the IRS set some clear guidance to help you determine if your home qualifies as a primary residence.

How to calculate basis of a primary residence converted to?

However according to [Reg. §1.165-9 (b) (2)] if the sale results in a loss the starting point for basis is the lower of the property’s original cost or the fair market value (FMV) at the time it was converted from personal to rental property.

When does the sale of a primary residence have to occur?

The rules state that both the residency term and the ownership term must occur within the last five years immediately preceding the sale of the home, but they don’t have to be concurrent. 4 The Section 121 exclusion isn’t a one-shot deal.