Do LLC owners have to pay unemployment tax?

Self-Employed Persons Sole proprietors, general partners, and members of an LLC treated as a partnership, do not pay state unemployment taxes on their self-employment income.

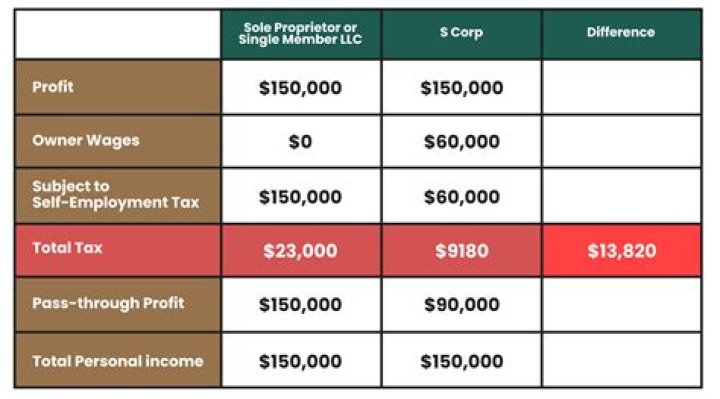

Can S Corp owner collect unemployment in Texas?

100% owner-shareholders of an S-Corporation who do not take a salary, LLC members who report self-employment income, and sole proprietors are among those ineligible to collect unemployment.

Do business owners have to pay FUTA?

Federal Unemployment Tax is due each year for every company that has W-2 wage employees. As the owner of an S-corporation, you are required to pay FUTA taxes for yourself, based on Internal Revenue Service compensation laws for your business structure.

Do business owners pay SUTA?

If you’re a small business owner with employees, rather than 1099 independent contractors, you are responsible for SUTA taxes. In the event you have employees in states that require employee SUTA contributions as well, you’ll need to withhold SUTA taxes from their wages. Not all small business owners pay SUTA taxes.

Who is exempt from FUTA and SUTA?

Most businesses are required to pay federal unemployment tax (FUTA) and state unemployment tax (SUTA). Certain organizations, including government employers, and nonprofit religious, charitable, and educational institutions are exempt from paying these taxes.

Does an LLC pay FUTA tax?

LLCs offer the tax benefits of both a (C or S) corporation and partnership. on wages paid to employees, and will file Form 940 (FUTA Tax return) and Form 941 (Quarterly Return for Income and FICA taxes) for amounts withheld.

What is exempt from FUTA wages?

Payments Exempt From FUTA Tax The payments include: Fringe benefits, which include the value of certain meals and lodgings, employer contributions to accident and health plans for employees, as well as employer reimbursements for qualified moving expenses.

Who pays SUTA employee or employer?

The State Unemployment Tax Act, known as SUTA, is a payroll tax employers are required to pay on behalf of their employees to their state unemployment fund. Some states require that both the employer and employee pay SUTA taxes. These contributions provide monetary support to displaced workers.

What percentage is FUTA and SUTA?

The employer also must pay State and Federal Unemployment Taxes (SUTA and FUTA). The FUTA rate is 6.2 %, but you can take a credit of up to 5.4% for SUTA taxes that you pay. If you are eligible for the maximum credit your FUTA rate will be 0.8%. The wage base for FUTA is $7,000.

Is a Futa return required for the owner of an S corporation?

As the owner of an S-corporation, you are required to pay FUTA taxes for yourself, based on Internal Revenue Service compensation laws for your business structure. As a working owner of an S-corporation, you must receive a reasonable wage from your company.

Do you have to pay Futa and Suta taxes?

Although FUTA and SUTA are different, and each state’s SUTA regulations and tax rates vary, the criteria that determine whether a company must pay FUTA and SUTA taxes are mostly the same. In most cases, if your company meets one of the two below criteria, you must pay FUTA and SUTA taxes:

How many employees do you have to have to pay Futa?

For example, if you have eight employees and you pay all of them at least $45,000 per year, you only need to pay the FUTA tax rate on $56,000 total – eight employees multiplied by the $7,000 FUTA cap).

Do you have to pay unemployment on a suta return?

State SUTA Tax Requirements All states require S-corporations to pay a separate state unemployment insurance. However, you’ll receive a federal credit of up to 5.4 percent for your state unemployment insurance payments on your FUTA return.