Do credit card debts get written off?

Generally, writing off some or all of your credit card debt is done through a debt solution. There are multiple debt solutions that can allow you to write credit card debt off, including: Individual Voluntary Arrangement (IVA)

Does debt ever get written off?

There is a common misconception that debts are written off after six years – but this is not true. Debts are not automatically written off after a certain amount of time. Common unsecured debts like credit cards, loans and overdrafts can become unenforceable after a limitation period of six years.

How long do you have to wait to write off bad debt?

If the debt is partially worthless, you have three years from the date you filed the original tax return, or two years from the date you paid the tax. If it was totally worthless, the IRS gives you seven years from the date of the original return and two years from the date you paid the tax.

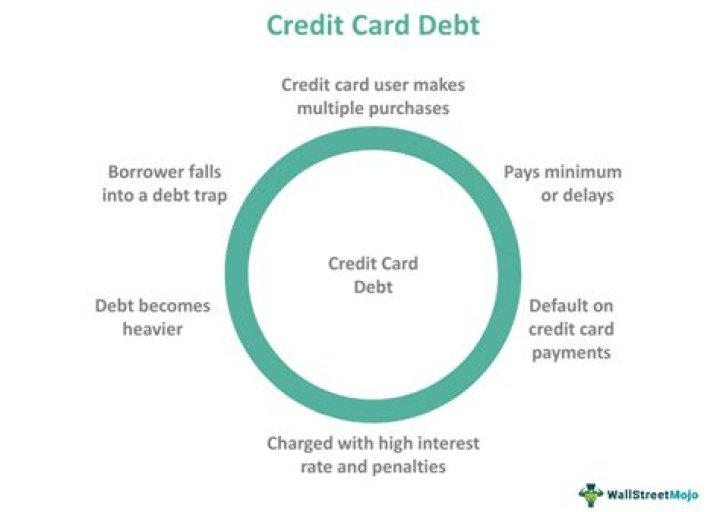

How to get out of credit card debt?

How to pay off credit card debt 1 Use a balance transfer credit card 2 Consolidate debt with a personal loan 3 Borrow money from family 4 Pay off high-interest debt first 5 Pay off the smallest balance first

What happens when you pay off your credit card?

Perhaps you canceled unused subscriptions and negotiated some other monthly bills, or simply resisted the splurge on that impulse buy. Congratulations, you finally paid off your credit card debt! So now what?

Which is the best credit card to pay off debt?

If you want a long stretch of time to pay off your debt, consider the Citi Simplicity® Card with 0% APR for the first 18 months on balance transfers (then 14.74% to 24.74% variable APR) or the Discover it® Balance Transfer with an introductory 0% APR for the first 18 months on balance transfers (then 13.49% to 24.49% variable APR).

What to do with high interest credit card debt?

After the high interest balance is paid off, you can start to tackle the debt on your balance transfer card more agressively. Similarly, if you’ve consolidated debt with a personal loan or loan from family or friends, prioritize paying off high interest balances first.