Can you still claim mortgage interest?

If you have or take out a home equity loan or line of credit and use the money to “buy, build, or substantially improve” your main or second home, the interest may still be deductible.

When can you not claim mortgage interest on taxes?

If the loan is not a secured debt on your home, it is considered a personal loan, and the interest you pay usually isn’t deductible. Your home mortgage must be secured by your main home or a second home. You can’t deduct interest on a mortgage for a third home, a fourth home, etc.

Can You claim mortgage interest on your tax return?

Essentially you can claim a mortgage interest deduction on your tax return for any expenses related to the interest paid on your mortgage. This has not changed in 2019; however there are some key nuances related to the deduction limits and standard deductions, including the following:

When do I have to pay 3 months interest?

Section 17 of the Mortgages Act (“Section 17”) provides that where a mortgage is in default a mortgagor is entitled to make payment of the mortgage amount upon payment of an additional three months’ interest or upon providing at least three months’ notice of the payment.

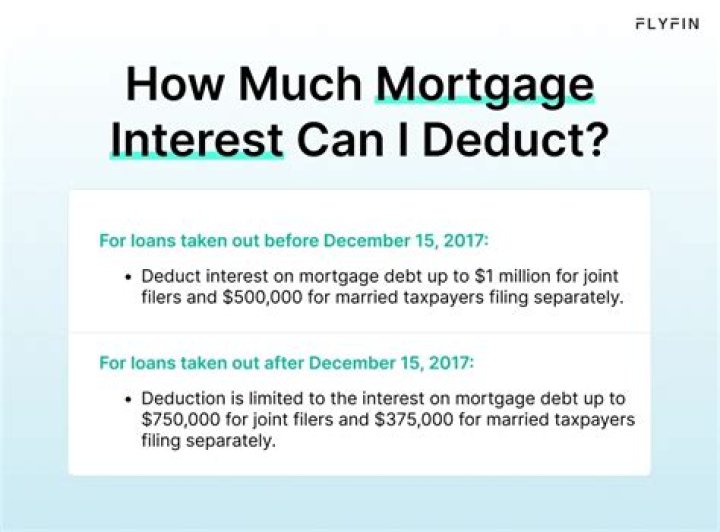

What’s the maximum amount of interest you can claim on a mortgage?

Together, the loans add up to $1.2 million, exceeding the $750,000 limit under the terms of the TCJA. You can only claim a mortgage interest deduction for the percentage attributable to the first $750,000 you borrowed. Interest associated with that other $450,000 is just money that you spent. You don’t get a tax break for it.

How can I maximize my mortgage interest deduction?

To maximize your mortgage interest tax deduction, utilize all your itemized deductions so they exceed the standard income tax deduction allowed by the Internal Revenue Service. The federal standard deduction is high enough that you’re unlikely to claim the mortgage interest deduction unless you earn a significant income.